The Endogenous Investor

Reflexivity, the Curve, and the Legibility Inversion

There’s a part of reflexivity that many venture LPs miss.

To see why, let’s start with the canonical Soros account. Karl Popper, his mentor at the London School of Economics, argued that knowledge advances through falsification. In other words, our understanding is always provisional. Soros, an economics student, brought that epistemological humility to markets. If participants are always operating on imperfect models of reality, their actions feed back into the reality they’re trying to understand. Mainstream economics — especially in its efficient-market and rational-expectations variants — tended to treat that feedback as second-order noise rather than first-order structure.

Soros called this reflexivity: a two-way loop where beliefs shape fundamentals and fundamentals reshape beliefs. Market sentiment about a bank’s solvency can make it insolvent. Causality runs in both directions, and the truth becomes a moving target. That bidirectionality is what made Soros’ insight useful: not as philosophy, but as a trading framework.

Venture has always run on this logic, but especially in today’s markets of capital legibility, narrative construction, and kingmaking. A certain platform firm’s industrialized content engine even published a playbook for it. Capital doesn’t just observe reality; it helps create the reality it claims to evaluate. Funding changes hiring, strategy, ambition, time horizons, and even identity. Narratives are not epiphenomena; they are inputs — and reputation often compounds faster than fundamentals. When investors anoint a company, they alter the probability space in which that company, its competitors, and even future founders operate. Capital doesn’t just follow conviction; it can manufacture it.

But while Soros’ theory focused on how market participants influence the assets they observe, venture capital reveals a second-order reflexivity: the loop doesn’t just affect markets. It reconstructs the participants themselves.

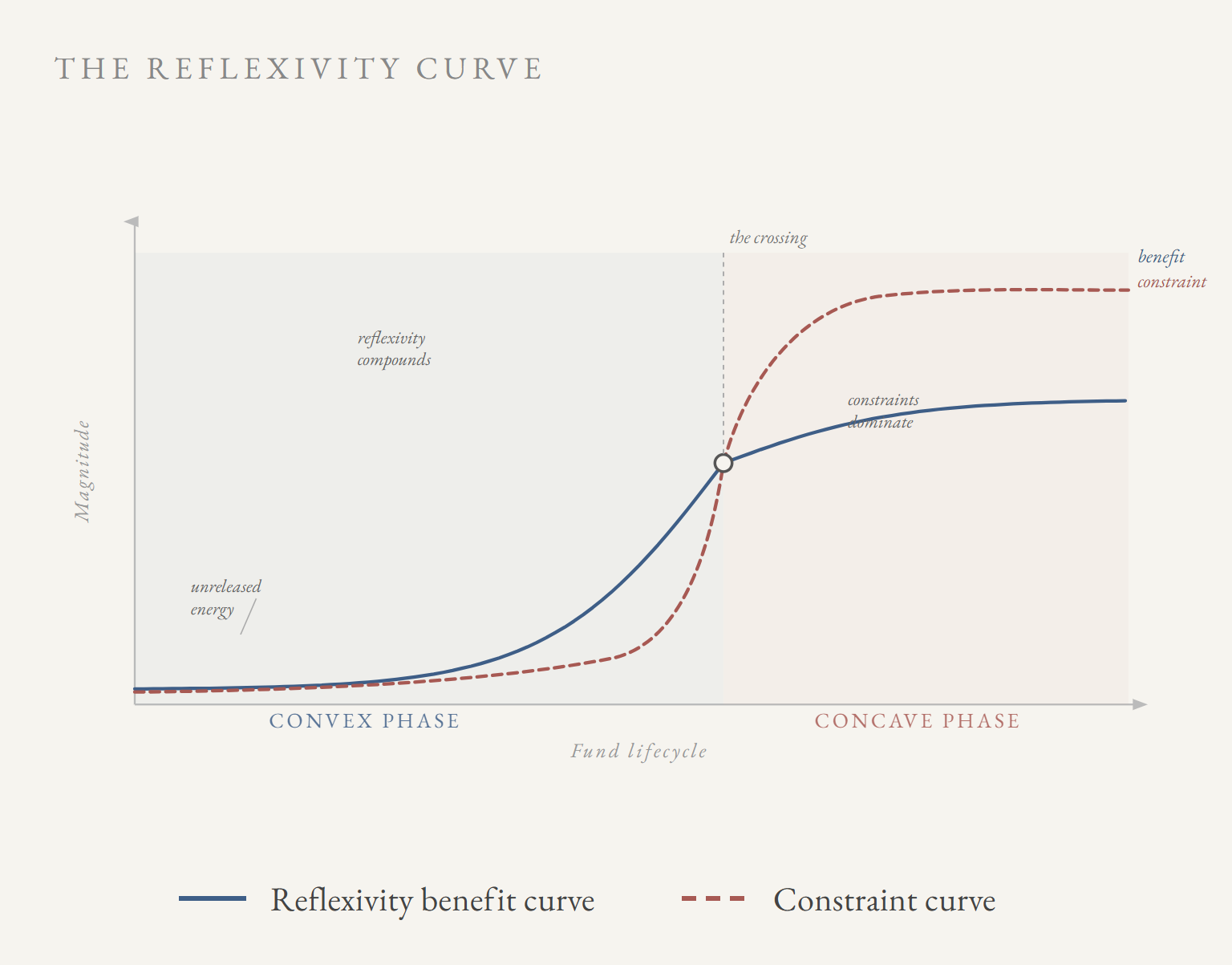

The Reflexivity Curve

In venture, reflexivity doesn’t stop at the startup or the market. It loops back over the firm. The GP is not a neutral observer of these dynamics but a participant absorbing them in real time, often without noticing. As firms create reflexivity for their portfolio through brand, narrative, and signaling, they simultaneously get shaped by it.

A strategy that succeeds becomes legible. Legibility attracts capital, deal flow, and attention. Those rewards then constrain future behavior, narrowing the firm’s ability to experiment or deviate from the script that made them successful. Over time, what began as an advantage becomes a selection pressure. Reflexivity stops being a tool the GP wields and becomes part of the environment that conditions them.

Think of it as two curves: reflexivity benefits that accrue steeply early and flatten, and a constraint curve that rises — sometimes slowly, sometimes all at once — until it crosses and dominates.

In the early stages of a firm — what I’ll call the convex phase — reflexivity is almost purely additive. The best GPs here aren’t just finding great companies before the market can see them. They’re actively compressing the distance between illegibility and legibility. Some do this deliberately: placing founders on the right stages, sequencing social proof, constructing the narrative frame that attracts downstream capital. Others do it implicitly, simply by virtue of their signal carrying weight. This dynamic is most potent when capital is scarce relative to opportunity: illegible companies, unformed markets, thin competition. Reflexivity expands optionality, until it doesn’t.

As the firm matures, a concave phase emerges. The GP’s brand becomes legible to LPs, embedding expectations about what the firm is meant to be. Capital has been raised against a story — sometimes against an illusion of learning — where markups are mistaken for returns and a rising tide for manager alpha. Strategy hardens into identity. The GP is no longer free to be interestingly wrong; they are forced to be defensibly safe.

The constraint runs deeper than narrative alone. Some of it is mechanical: AUM has gravity, and as it compounds it pulls the firm toward larger rounds, more legible companies, deeper buyer pools. The math of deployment hardens into path dependence.

Some of it is environmental. The arbitrage windows that built the firm are closing, sometimes because the market caught up, sometimes because the firm’s own success made the thesis too legible to remain scarce. In that arena, multiple well-resourced firms are running their own versions of the reflexive playbook on the same companies. The reflexivity that built them doesn’t disappear. It gradually shifts from being a weapon to becoming a ceiling. The firm becomes pinned to a local peak.

The endpoint is a legibility inversion. Early in a firm’s life, illegibility is a liability. The GP must struggle to make unconventional ideas legible to capital and to win over founders without a brand to lean on. Later, legibility becomes the liability. Success, perceived or real, attracts capital, and with it the diseconomies of scale and compressed returns. The GP moves from the illegible alpha of the explorer to the legible beta of the institution.

A handful of firms have attempted to resist this inversion. For example, Benchmark through fund size discipline and an equal partnership structure (which requires partners willing to forgo the economics of scale), Founders Fund by institutionalizing contrarianism itself (which risks becoming its own form of legibility). Each illustrates the difficulty as much as the possibility: the same moves that delay any form of decay come with tradeoffs of their own.

For GPs, success expands the firm’s economic base. Larger funds increase management fee revenue, smooth personal volatility, and justify broader infrastructure. From a firm-building perspective, raising more capital is rational. It reduces fragility. It professionalizes operations. It attracts talent.

For LPs, allocating to established franchises reduces career risk. A commitment to a widely respected firm is easier to defend internally than backing a small, illegible manager whose thesis may take years to validate. Institutional governance is built to favor legibility. Brand becomes a proxy for safety.

The reflexivity curve reframes how a firm should be evaluated. Most allocation frameworks are static: track records, quartiles, brand, team pedigree. Snapshots of past outcomes. But reflexivity is dynamic. It changes the conditions under which those outcomes were produced.

The relevant question is not whether a GP once generated alpha, but whether the conditions that made that alpha possible still exist. What matters is where the firm sits on its own curve: whether it remains coiled with unreleased energy, or whether scale, identity, and legibility now dominate decision-making.

From this perspective, an LP’s risk is not in underwriting managers without long histories. It is allocating statically in a dynamic system, institutionalizing yesterday’s edge at tomorrow’s prices.

***

Thanks to Rafael, Tom, Matt, Jason, and my team for feedback.