Reasoning in Regime Changes

Reasoning in non-ergodic systems

In Criticality Investing, we discussed how real‑world markets are self‑organized criticality systems. By this, we mean that they are self‑tuned to be at the edge between order and chaos. As such, these systems exhibit path dependence (early events constrain the space of future options), long memory (persistent lock‑in from past states), and naturally lead to metastable states (systems can get trapped in regimes that appear stable but can change quickly).

We explained that systems in metastable states build up latent tensions that are released with an exogenous and/or endogenous catalyst, placing the system in a new metastable state and often ushering in a large capital rotation. A canonical example is ChatGPT’s launch in 2022, which created a massive capital rotation and a subsequent datacenter CapEx cycle. Before ChatGPT the market was in a “SaaS-first mindset”, while several latent tensions existed:

Research labs knew that increasing data, parameters, and compute would reliably improve model performance, but most of this lived in papers, APIs, and demos rather than a mainstream product narrative.

Foundation models were already showing emergent capabilities (few‑shot learning, code, and reasoning) that exceeded the mental models most enterprises and investors had (i.e. “ML is just a feature”), thus creating a gap between observed technical potential and commercial adoption.

Demand for GPU‑class compute was accelerating but was still framed as research or niche workloads; the hardware and cloud ecosystems had not yet re-rated around AI as the primary driver of datacenter CapEx.

There was an unresolved debate about whether AI would be a horizontal capability inside software or a new platform layer with its own economics, but no canonical product yet existed to anchor either direction.

The US–China semiconductor cold war was already brewing around advanced chips and export controls, with AI as an implicit driver of demand and national-security concern, but without a public AI moment to crystallize it.

If we use AI as an example, criticality shifts can clearly translate into high‑convexity outcomes when capital is well positioned ahead of the transition. But why can’t most investors see these latent tensions in advance?

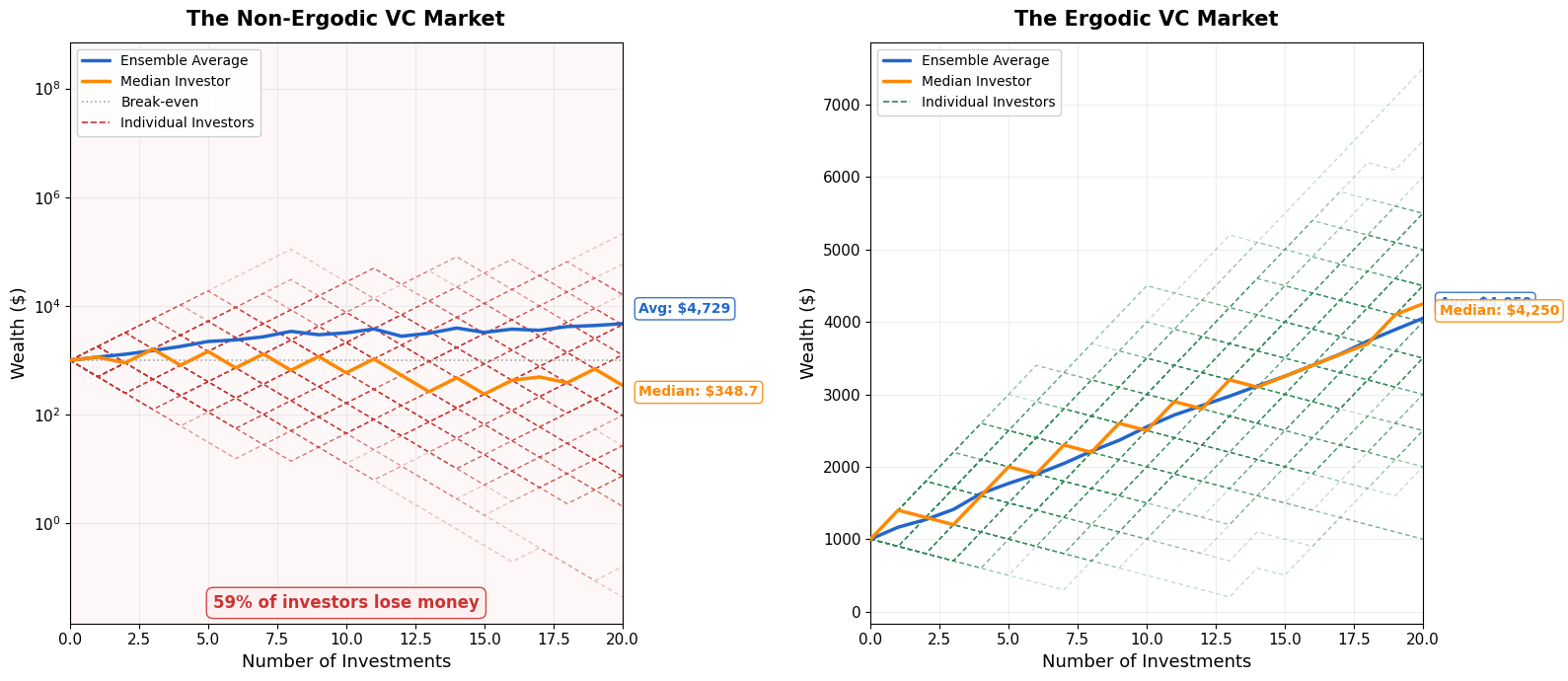

Because the result of path dependence, memory, and absorbing/metastable states means that real‑world markets are non‑ergodic. In an ergodic system, long‑run time averages along one trajectory are equal to ensemble averages. For instance, in a fair coin flip process, over a long enough sequence the fraction of heads along one person’s time series converges to 50%. That matches the 50% you get by averaging across many independent coin‑flip sequences. In non‑ergodic systems, history matters, not all states are explored, and time averages along a single trajectory can differ sharply from ensemble averages. For example, a gambler betting repeatedly may appear profitable on average across many scenarios, but in reality will likely go bankrupt and stay there, so the realized outcome is much worse than the average suggests..

One way to think about non‑ergodic systems is in the context of a Markov chain in which transient states (white circles) feed into absorbing states (black circles, like states 4 and 5 below) that trap the system and prevent it from fully exploring the state space.

In VC, for example, this means that an investor’s long‑run portfolio return can diverge sharply from the cross‑sectional average, which is driven by a handful of outlier funds.

Non‑ergodic (left): The ensemble average looks great on paper (because the power law means a few investors hit extreme right-tail outcomes). But the median investor’s wealth collapses and ~59% of investors lose money. The few massive winners drag the average up while most go broke. This is multiplicative dynamics (repeated percentage gains/losses)—what happens to the typical VC investor diverges wildly from the average. Ergodic (right): Ensemble average ≈ median. Every individual’s trajectory clusters around the mean and the time average and the ensemble average converge.

Non‑ergodicity means that systems and markets undergo regime changes, when catalysts kick the system out of metastable states. During a regime change, volatility spikes and the system eventually settles into a new metastable state. In the Markov chain example above, a regime shift means small changes in transition probabilities (the weights on the edges) suddenly make it much more likely that the process ends up in a different metastable state, effectively moving the system from one long‑run pattern to another. In some cases, the whole structure or topology of the chain itself changes. When this happens, historical observations become much less useful in predicting the future because we are effectively in a ‘new world’.

How should investors make decisions in complex, non‑ergodic markets?

The answer is to go deeper.

Applying a Bayesian inference lens, let’s assume that everything we know is encoded in a prior over possible models of how the market works—its transition probabilities, payoff structures, and latent regime states. Historical data then updates that prior into a posterior over models.

But when the regime shifts, the generative model itself may change, so we are no longer simply updating beliefs about states within a fixed model; we are now uncertain about the model itself.

So deeper pattern recognition is needed to detect when the structure generating outcomes has shifted—when small anomalies or surprises are not noise within a regime but signals that transition probabilities, payoff functions, or even the state space itself have changed. At that point, the task is no longer to extrapolate from the historical realized path, but to infer the most plausible underlying mechanism that may be producing the new observations. In other words, we must move from updating beliefs within a model to constructing new models of reality. We believe, practically, this means asking mechanism-based questions vs analogy-based questions, for instance:

Value creation: What are the new underlying dynamics of value creation, versus simply asking whether this fits prior economic frameworks like CAC/LTV?

GTM dynamics: What do current data points imply in terms of distributional advantages and feedback loops, versus just asking whether the observed network effects look like prior winners?

Regime Invariance: Which elements of competitive advantage are regime-dependent (e.g., capital availability, GPU scarcity) versus regime-invariant (e.g., switching costs, workflow lock-in)?

Founder adaptability: Is the team built to navigate continuous regime shifts, or are they optimized for execution within the static playbook that is currently working?

Market structure: What structural conditions, customer behavior, procurement dynamics, integration advantages, must persist for this company to sustain margins and avoid commoditization?

The aim is to construct a model of the current state of the world—a causal or structural model that makes sense of what we are seeing and is grounded in underlying mechanisms. Otherwise, the danger is that we either rely on momentum and consensus opinions or apply a world model that is no longer relevant to the new regime.

In a future post, we will discuss our views on the current market and the nuances of pattern recognition by induction and abduction in the context of causal or structural models of complex markets.